Anyone needs to be aware of the scale of values to which most people in Western countries refer. It serves to have a more straightforward path of life and, consequently, set one’s goals.

In 1943 behavioral scientist Abraham Maslow wrote that a “hierarchy of needs influences humans worldwide”

His “A Theory of Human Motivation” organizes human needs across five levels, where the ones in the lower end must be satisfied before progressing onto the next level. In the beginning, there are physiological needs such as sleep and shelter, while on the other there are esteem and self-realization.

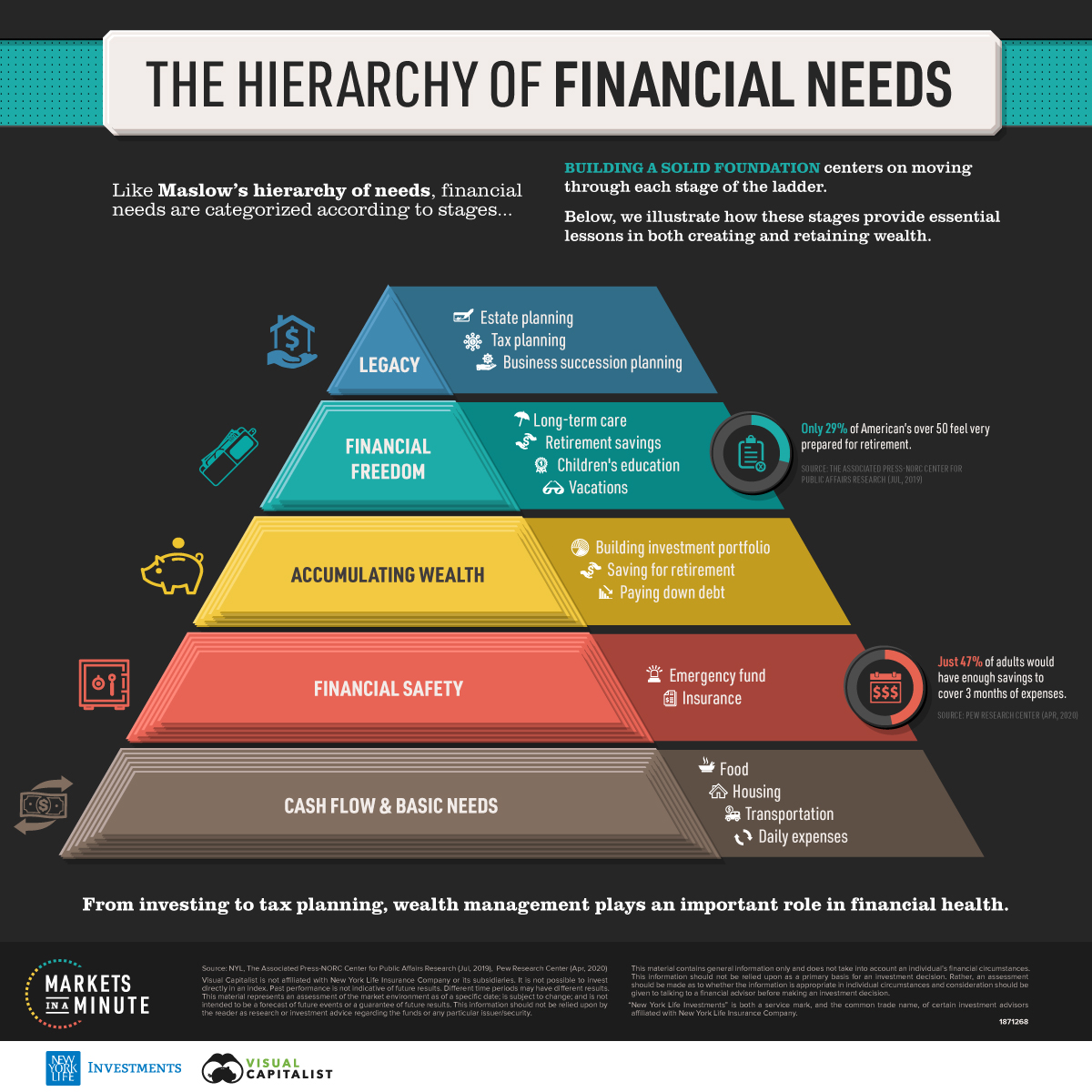

This graphic explores how Maslow’s theory applies to our financial needs, pinning down the steps to creating a solid financial foundation (Minute chart from New York Life Investments).

The Financial Needs

What are the five levels in the hierarchy of financial needs?

- Cash flow and basic needs

Covering food, housing, and daily expenses. Ensuring the fundamentals, including our physiological needs, are protected financially.

- Financial safety

This covers insurance and an emergency fund to help prepare for unforeseen events and risks. As a safety cushion, an emergency fund should cover three months of living expenses in case of an accident, an unexpected health or family issue, or losing a job.

- Accumulating wealth

This includes growing investments, paying down debt, and saving for retirement. At this level, the focus shifts to increasing assets for long-term success and longevity.

- Financial freedom

Long-term care and children’s education are found within this category, along with retirement savings and vacations. These financial needs are linked with esteem needs, such as self-respect and personal accomplishment.

- Legacy

Estate planning, tax planning, and business succession planning all fall within this category, connecting with self-actualization in Maslow’s pyramid.

Moving along this path can help create an enduring roadmap for your financial health. This as a general rule, even if financial needs can shift based on a given situation.

Financial Needs Highlights

It’s easy to describe the theory in concept, but how does it impact our day-to-day lives in practice?

As individuals live longer, many are focused on longevity risk and concerned with having enough savings for retirement—across all income levels.

For Americans in the lower income bracket, 50% worry about their retirement savings, while 26% worry in upper-income levels.

| Worry about each of the following often | Lower Income | Middle Income | Upper Income |

| Being able to save enough for retirement | 50% | 37% | 26% |

| Paying their bills | 59% | 35% | 15% |

| The amount of debt they have | 51% | 35% | 21% |

| The cost of health care for them and their family | 47% | 35% | 18% |

| Take a pay cut due to reduced hours or demand for their work | 51% | 25% | 18% |

| Losing their job | 40% | 21% | 11% |

Source: Pew Research Center, survey of U.S. adults conducted April 7-12, 2020

Debt is also a primary concern among many Americans, as the cost of both healthcare and education have continued to rise. Average annual college costs, for example, have risen 25% over the last decade, while U.S. household debt has roughly doubled to $14 trillion since 2004.

Only after these above needs are taken care of, people can focus on the top of the financial needs, taking care of legacy-focused items such as estate and tax planning or business succession planning.

Your Financial Plan

It is crucial to have a reliable financial plan.

Especially during times of uncertainty, people need to have a clear plan that accounts for changing life circumstances, such as a new job or purchasing a house. But it must also consider the rungs of the ladder and how to change tactics to pursue your financial goals better.

Having a better awareness of financial needs can help people make more informed choices from day-to-day purchases to long-term investment decisions.

For this reason it is essential to have an expert advisor next to you to accompany you over the years. It is a very specialized field that requires vision, experience, competence, know-how.