Accumulation

Voluntary Plan

A voluntary accumulation plan is an investment method in which a retail investor periodically invests (at their discretion) relatively small amounts of money, building a large position over an extended period. This can be an excellent solution for anyone who wishes to build a capital but is not in a position to invest a large sum of money at one time.

A winning strategy

An accumulation plan is an investment strategy that can help investors increase the value of their portfolios. It is one of the best and straightforward strategies to put into practice in a long-term perspective.

A strategy consists of a set of principles designed to achieve your financial and investment goals. It is based on the investor’s goals, risk tolerance, and future capital needs.

These plans are often ideal for the small investor who does not have a large sum to invest upfront but can plan a certain amount of money each month for the investment. People will use these plans to achieve long-term goals, such as investing in a child’s retirement or college education.

The strategy adopted can frustrate or maximize results with the same money set aside regularly over the years. Strategy is not a simple choice.

Mentoring

Investing is complex. Do-it-yourself generally causes damage (loss or lesser results). To make it simple, you need an expert, an authorized financial advisor who will carefully choose who will set you the investment strategy appropriate to your goals and then accompany you over time to update it as often as necessary because it will change the world, but also your goals.

Advantages

- It is flexible because it can be interrupted at any time if necessary

- It is protective because it disconnects the investor from the reality of the market, thus avoiding being subjected to that often irrepressible psychological and emotional component that pushes investors to buy an instrument when it rises, and to sell it when it falls, also based on past returns.

Risk protection

The accumulation plan offers the advantages of the average dollar cost, which allows you to reduce the impact of the expected volatility typical of the stock market, increasing your overall earnings.

It is a method – widely used in managing personal finances by the most astute people – which consists of paying small amounts into your investment account every month.

This method allows you to balance the quantities bought each time according to the value of the moment, rebalancing the natural highs and lows of the stock market.

The investor will buy more shares when the price is lower and fewer shares when the price is higher. Therefore, the average dollar cost results in a lower average cost per share and reduces risk by allowing investors to offset short-term volatility.

It is the best choice to support your investment by containing risks.

Main features

- Diversification in order not to take specific risks.

- Long time horizon, mainly if we use shares because history has shown that the risk decreases by increasing the duration (see a section dedicated to actions).

- Ease of investment is another benefit as investors can set up the plan and invest automatically every month.

How it works

The repetition of small investments in the long term means that these are linked to the growing world rather than the stock market’s performance. The broader the time horizon, the more this concept is true.

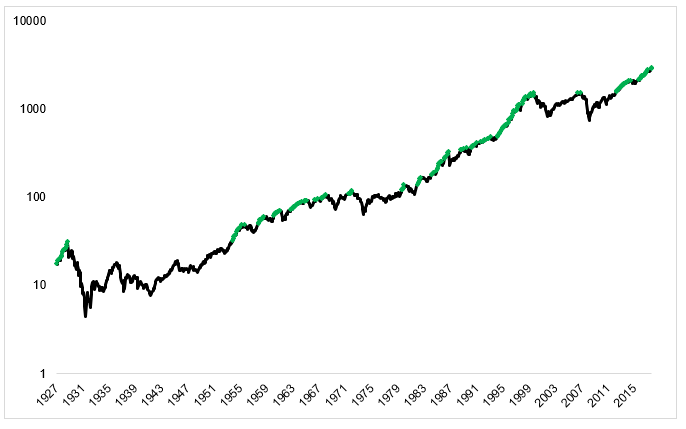

So the maximums and minimums no longer have relevance because when it refers to the growing world, we have a progressive path that rises where there is no maximum. All this is well represented in the graph of the American S & P500 stock index, from 1927 to the US, which shows the process of growth and value creation, with 202 points of maximum monthly.

So why bother with something that happens so often? It is more of a regular event than an exceptional one.

The history of the S & P500 index tells us that new highs always follow new highs! The returns at 3, 6, 12, and 24 months, following a maximum point (All-time high) of the American stock exchange, were on average positive and therefore led the index to a new high.

Therefore, the cadenced investment takes away the importance of the day in which it occurs because, in the long run, it will, in any case, be higher and higher because the world goes on.

In addition to being a helpful tool for achieving personal and family goals, the CAP is an excellent alternative or integration to the pension fund. It allows small amounts to be freely and constantly set aside a reasonably long period into a fund that can be redeemed upon retirement or reinvested to generate an annuity.

Life-vest

For those who are not lucky to have significant capital to invest, the CAP allows you to start building a dream or peace of mind, with any amount, even with only 5% of a small income. Those who do not accumulate do anything concrete for themselves, and start is already an important fact. The key, however, will be continuity over time, which is the determining factor because the sum of small amounts invested can give excellent results.

You know how to be rich

It is an excellent solution that allows to profit from the monthly savings, in a way proportionate to needs and gradually. In addition, the gradual investment reduces the risk associated with market timing (it isn’t easy to know exactly what is the best time to invest), obtaining a better price as it is mediated over time.

- According to its income, capacity, and willingness to spend, FLEXIBILITY the amount to be invested is chosen, also in the light of the objectives.

- LESS RISK the gradual entry and the monthly maturity allow limiting the inconveniences related to investment timing and volatility.

- CUSTOMIZED TIMES the flexibility of the Cap is not only in the figures but also in the timing, with wide margins. However, there is a tendency to use this solution for medium-long horizons.

- EXPLOIT OPPORTUNITIES Allows you to position yourself on market opportunities even if you do not have the substantial initial capital.

- PLANNING is the ideal tool for planning long-term goals for yourself and your family.